Related Articles

An employer-sponsored 401(k) retirement plan can have many benefits for your employees and your business.

- Offering a 401(k) plan can help small businesses meet increasing employee expectations and retain top talent.

- Companies that offer 401(k) plans are eligible for significant tax breaks and deductions.

- Both businesses and employees benefit from optional employer contributions to workers’ 401(k) accounts.

- This article is for business owners who want to know why they should offer a 401(k) plan.

If you’re like many small business owners, you’ve probably asked yourself whether you should offer a 401(k) plan as part of your employee benefits package. You’ve probably also asked yourself what you and your company stand to gain from such a move and which employees will benefit from it. We’ll break down how 401(k) retirement savings plans provide advantages for both employers and employees.

Editor’s note: Looking for the right employee retirement plan provider for your business? Fill out the below questionnaire to have our vendor partners contact you about your needs.

What benefits do employers get from offering a 401(k) plan?

401(k) plans are funds that allow employees to contribute a portion of their wages to save for retirement.

“Any business can set up a 401(k), a salary deferral plan to which employees can contribute part of their salary and have it not count as income on their W-2,” said Christian Brim, CEO of financial firm Core Group. “And oftentimes, businesses with fewer employees benefit most from them.”

Here are some of the advantages for employers:

Attractive benefit to recruit and retain talent

Retirement benefits are increasingly important to job seekers. Many workers ask during the job application process whether a company has a retirement plan such as a 401(k), and they seriously consider the availability of such a plan when deciding whether to accept or remain in a job.

“There can also be big financial benefits from a 401(k) in helping to retain and attract top talent and the associated cost savings and productivity gains,” said Stuart Robertson, CEO of ShareBuilder 401k.

Robertson’s research shows that replacing an employee costs 29% to 46% of an employee’s annual salary, depending on whether that team member is in a managerial position.

“It’s estimated that an employee who earns $50,000 a year can cost $14,500, on the low end, to replace,” he said. “A 401(k) plan is a small price to pay, not only for retirement but also for building and keeping a great team.”

Did you know?: While a 401(k) is a retirement vehicle, employees can also borrow against a 401(k) as an asset, giving them some leverage should they need an infusion of liquid cash without incurring tax penalties.

Better work ethic

Brian Halbert, founder of Halbert Capital Strategies, said his clients have reported significant increases in worker loyalty and productivity when they have added a 401(k) plan to their employee benefits packages.

“The single largest benefit coming from a 401(k) is financially wise employees that have a zeal for working hard for their company,” Halbert said. “Oftentimes, we see the ROI in productivity and loyalty.”

Lower tax liability

Business owners with employees can contribute a hefty portion of their own salary to their personal 401(k) account (the one associated with the plan they offer to workers), possibly putting them in a lower tax bracket. In 2022, that sum is up to $20,500 tax-deferred for employers under age 50 and up to $27,000 for employers age 50 or over.

Business tax credits

The SECURE Act (Setting Every Community Up for Retirement Enhancement), signed into law in December 2019, increases tax credits for businesses implementing a first-time 401(k) plan. The act increased tenfold the tax credit companies with one to 100 employees can claim for qualified setup and administrative costs associated with startup 401(k) plans.

Before the SECURE Act, the tax credit for the first three years of an employee 401(k) plan was 50% of qualified startup costs, not to exceed $500. Those costs included – and still include – the cost to set up and administer the plan and to educate employees about it.

Under this law, however, small businesses now get a 401(k) startup credit whose limit is either the greater of $500 or (a) the lesser of $250 multiplied by the number of non-highly compensated employees (HCEs) eligible for plan participation or (b) up to $5,000.

The IRS defines an HCE as an employee whose salary was more than $130,000 in 2021 and more than $135,000 in 2022. Robert Pyle, owner of Diversified Asset Management, said the more HCEs a business has, the higher the tax credit. The maximum tax credit, which can be claimed for three years, is $5,000.

Adding an automatic contribution feature to a new or existing 401(k) plan yields another tax break: $500 for each of the first three years in which the feature is available. This feature, also known as automatic enrollment or auto-enroll, lets employers automatically enroll eligible employees in the plan unless the employee affirmatively elects not to participate in it.

Business tax deductions

Many employers make matching contributions to employees’ 401(k) accounts. These contributions may qualify as ordinary business expenses, in which case they are tax deductible up to the annual corporate deduction limit on all employer contributions (25% of covered payroll). Profit-sharing contributions to employees’ 401(k) accounts are also deductible, further reducing the tax liability for small businesses.

Key takeaway: Providing a 401(k) plan can help companies recruit employees and save on business taxes. Self-employed 401(k) plans allow independent contractors and sole proprietors to save for retirement as well.

What are the advantages of 401(k) matching?

While businesses aren’t required to offer a 401(k) contribution match for employees, it’s still a good idea. Robertson said matching contributions can boost employee morale and, because they are deductible, drive down a business’s tax liability.

If you want to offer a matching program but you’re afraid some employees will just take the money and run, consider a vesting schedule. With this arrangement, employees can’t take the employer’s contributions until the employees have participated in the retirement plan for a certain length of time.

For example, employer matching contributions might not fully vest for three years. If an employee leaves for another job before those three years are up, they aren’t entitled to all of the contributions the employer has made on their behalf. Of course, they do get to take all of the money they have personally contributed.

Some companies opt for profit-sharing contributions to employees’ 401(k) accounts when business is good. As mentioned above, these contributions are also tax deductible.

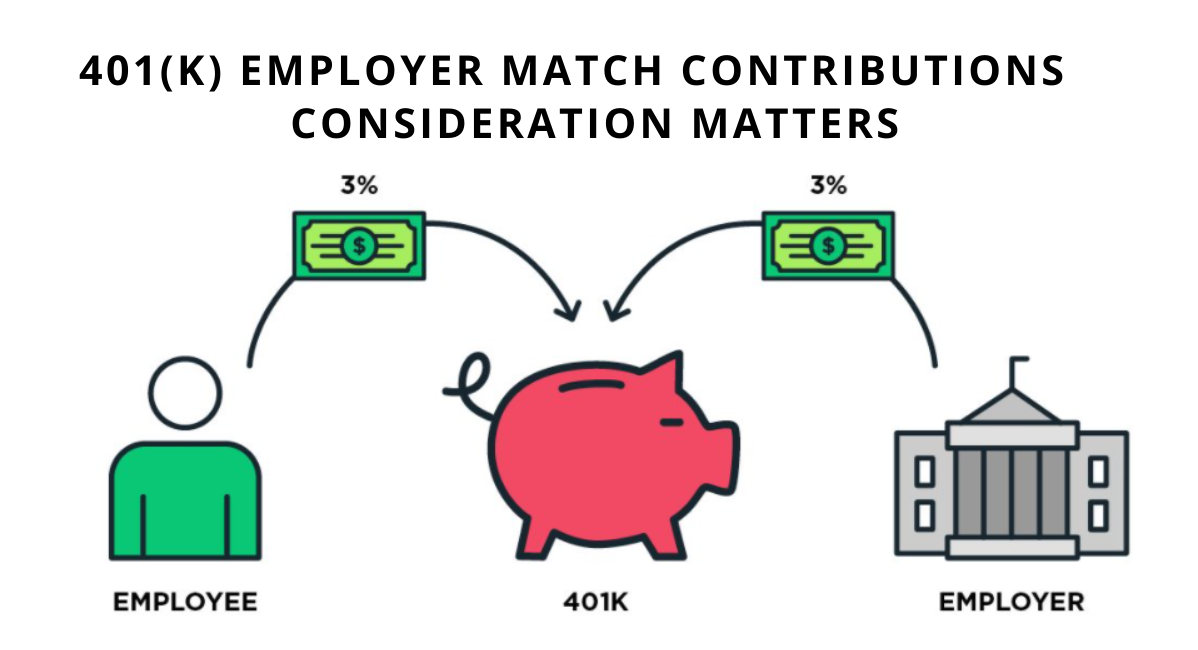

“The typical 401(k) match is called a safe harbor nonelective match of 3% of [the employee’s] salary,” Pyle said. “This means the employees get 3%, whether or not they participate in their employer’s 401(k) plan. Other match types are 100% on the first 3% of salary deferred and 50% on the next 2% of salary deferred.”

Did you know?: Some of the best payroll software providers, such as ADP and Paychex, offer 401(k) plan services as part of their packages.

How to start offering a 401(k) plan

Once you’ve decided to offer a 401(k) plan to employees, you’ll need to follow these steps to ensure compliance:

1. Document the 401(k) plan.

The first step you’ll need to take once you decide to offer your employees a 401(k) plan is to document the plan details. This process can be tedious, and small business owners often outsource this task.

Your plan should include details about contribution amounts, benefits payment timelines and eligibility information. Once you create the plan, you’ll have to submit it to the IRS for approval. Also, remember to review this plan annually to remain in compliance.

2. Open a trust.

Once your 401(k) plan has been approved, you’ll need to set up a trust account where all plan assets will be held. At this point, you’ll also need to select a trustee who can oversee all plan activities, including contributions and distributions.

3. Implement a recordkeeping system.

The next step is to implement a system to track plan values and employee contributions. If you need assistance with this step, consider hiring a recordkeeper.

4. Update participants on plan changes.

The IRS requires all business owners to consistently update 401(k) participants on changes, investments and associated fees. Business owners are also required to provide employees with a summary plan description, including detailed information about how the plan operates.

Tips for implementing a 401(k) plan

If you decide to offer a 401(k) plan, keep these tips in mind:

1. Consider outsourcing the administration.

Bringing in an in-house expert can be very costly, and doing so without experienced personnel could lead to mistakes or inefficiencies. By outsourcing, you improve efficiency and reduce liability.

Professional employer organizations (PEOs) are third-party companies that handle human resources, payroll, benefits and 401(k) plans for small businesses. Thousands of small businesses nationwide partner with PEOs to access competitive benefits and 401(k) plans.

Choosing a PEO can be complicated, but several types make sense for small businesses. The best PEOs have industry accreditation, minimal requirements for coverage, and great features, including short-term contracts.

2. Provide competent, qualified financial advisors.

It’s very beneficial for your employees to have someone to consult when they have questions about how to invest in their account and how much they should contribute. An advisor takes the burden of providing financial advice to your employees off of you. Be sure to properly vet your applicants for the financial advisor position, because poor financial advice can have serious financial and legal consequences.

3. Provide good investment options.

Ensure your company offers a good range of investment options. Your mutual fund options should represent different markets, such as U.S. stocks, international stocks and bonds. A good rule of thumb is that 75% of your mutual funds should have an expense ratio of less than 1%.

Also, keep track of how the funds in your plans are doing to see whether they are underperforming, matching or outperforming their benchmarks. You want to ensure your employees are happy with their options. It should be simple and free to swap fund options.

Key takeaway: To run your 401(k) program in a compliant, budget-friendly manner, consider outsourcing benefits administration, provide reliable consultants and offer good investment options.

What are the best small business 401(k) options?

Not every 401(k) plan is built for large corporations. As a small business owner, you have options for plans that fit your budget and business goals. Here are some of our top picks:

Guideline

Guideline is a top employee retirement plan provider that handles all of your 401(k) plan needs, including plan administration, investment management and recordkeeping. The company charges a monthly base fee and a per-participant fee.

ShareBuilder 401(k)

ShareBuilder 401(k) is a great option for employers offering a safe harbor 401(k) plan. The company provides small businesses with a plan administrator, custodian, investment advisor and recordkeeper. Contracts are not required, so you can cancel at any time.

Paychex Employee Retirement

Paychex offers 401(k) plans that integrate with its HR, payroll and employee benefits services. Business owners can choose their own 401(k) plan, IRA, 403(b) and investment options to offer employees, as well as add their preferred financial advisor or plan design. Paychex makes it easy to set up your plan and integrate with automated payroll to handle employee enrollment and contributions.

Human Interest

Human Interest offers user-friendly 401(k) plans and provides cost-effective employee retirement options to small businesses. Human Interest’s benefits start at just $120 per month, plus $4 per employee per month, including full recordkeeping, administration tools and seamless payroll integration.

American 401k

American 401k is a small retirement benefit services provider that offers highly personalized service combined with the backing of a large national insurance company (MassMutual). Small business owners who want a no-frills, no-fuss employee retirement package can work with American 401k to design the perfect plan for their needs.

ADP Employee Retirement

ADP’s employee retirement benefits complement the company’s payroll services through an all-in-one platform. The employee retirement benefit accounts are cost-effective and easy-to-use solutions for small businesses with at least a couple dozen employees.

Vanguard

Vanguard is best for entrepreneurs who want a solo 401(k) plan. There are no setup fees, and you can choose from more than 100 investment options. The company’s website includes various tools to help you decide where to invest your money.

The 411 on 401(k) upsides

Retirement plans are a great way for employers to attract and retain top talent. Employers should also consider the tax benefits of offering a 401(k) plan, particularly the advantages of matching employee contributions. To ensure compliance, businesses must evaluate the hours of full- and part-time employees when determining who is eligible for company-sponsored retirement plans. But by following the tips above, you’ll reap the rewards of offering this valuable retirement benefit to your employees.

Read & Write : write for us